Quebec Car and Home Insurance Premiums Rise Again in 2026

Quebec residents renewing their car or home insurance policies in 2026 continue to face a familiar reality: insurance premiums are still rising.

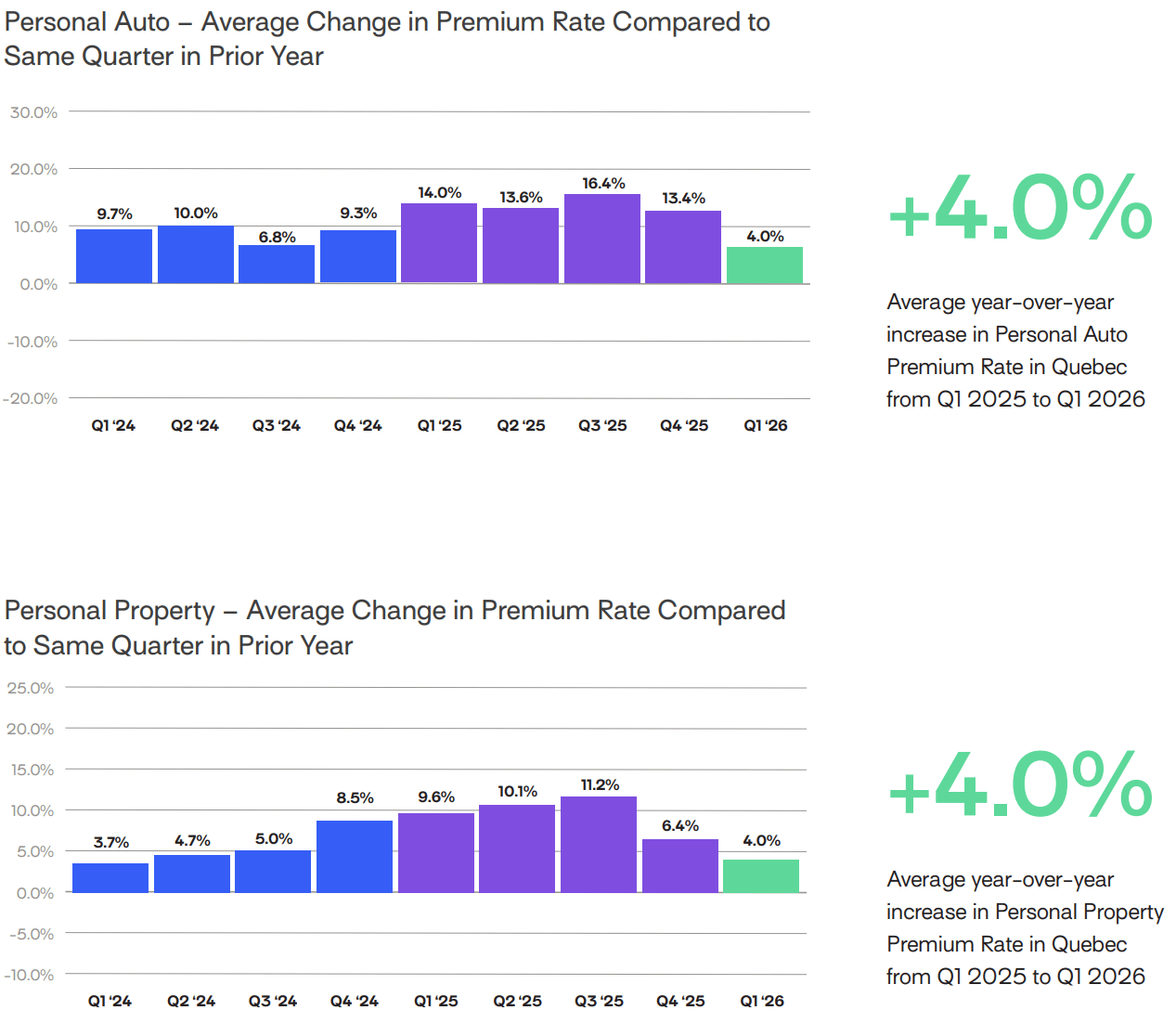

According to the latest edition of the Applied Rating Index, personal auto insurance and home insurance premium rates increased once again during the first quarter of 2026. While Quebec remains one of the least affected provinces in Canada, consumers are not immune to the rate increases being observed across the country.

The good news? The data suggests that the pace of premium increases is slowing compared to what was seen in 2025.

Key Takeaways

*Increase from Q1 2025 to Q1 2026.

- Quebec auto insurance: +4.0%

- Quebec home insurance: +4.0%

- National auto insurance increase: +11.1%

- National home insurance increase: +8.6%

- Quebec remains among the least affected provinces

- Premium increases are slowing compared to 2025

Insurance Premiums Continue to Rise in Quebec

According to the Applied Rating Index for the first quarter of 2026, personal auto insurance premium rates in Quebec increased by 4.0% compared to the first quarter of 2025. Home insurance premiums also increased by 4.0% over the same period.

Although these increases may appear modest compared to those seen elsewhere in Canada, they still represent additional pressure on household budgets at a time when many Quebec families continue to face a higher cost of living.

* Source: Applied Rating Index – Q1 2026

Quebec Is Holding Up Better Than the Rest of Canada

Compared to other Canadian provinces, Quebec continues to experience relatively moderate insurance premium increases.

| Province | Auto Insurance | Home Insurance |

|---|---|---|

| Alberta | +21.3% | +16.2% |

| Ontario | +11.8% | +6.2% |

| Atlantic Provinces | +9.6% | +10.8% |

| Quebec | +4.0% | +4.0% |

Alberta remains by far the province most affected by rising insurance costs, with personal auto insurance premiums increasing by more than 21% year over year. At the other end of the spectrum, Quebec recorded the smallest increase among the provinces analyzed.

Several factors help explain this situation, including Quebec's unique automobile insurance system, a highly competitive insurance market, and generally lower claims costs compared to some other regions of the country.

Why Are Insurance Premiums Still Rising?

There is no single reason behind the continued increase in insurance premiums. Instead, multiple economic and operational pressures continue to impact the insurance industry.

Inflation and Rising Repair Costs

Although inflation has eased from the peaks experienced over the past few years, repair costs remain elevated.

Insurance companies continue to absorb higher costs for auto parts, building materials, skilled labour, and professional services related to claims handling. As a result, each claim costs significantly more today than it did only a few years ago, putting direct pressure on insurance premiums.

Vehicles Are Becoming More Complex and More Expensive to Repair

Modern vehicles are equipped with advanced technologies such as cameras, radar systems, proximity sensors, and driver-assistance features.

While these innovations improve road safety, they also significantly increase repair costs following even a minor collision. Replacing a simple bumper may now require recalibrating multiple electronic sensors, dramatically increasing repair bills.

Extreme Weather Events

Home insurers must also contend with a growing number of severe weather events.

Floods, windstorms, hailstorms, wildfires, and other natural disasters generate billions of dollars in insurance claims across Canada every year. Although Quebec is generally less exposed than some Western Canadian provinces, climate-related losses continue to place upward pressure on home insurance costs.

Auto Theft Remains a Major Challenge

Vehicle theft continues to impact the insurance industry across Canada.

Major urban centres such as Montreal, Laval, and the Greater Montreal Area remain particularly affected. Insurers must absorb not only the cost of stolen vehicles, but also investigation expenses, replacement vehicles, and associated claims costs.

Growing Competition for New Customers

A lesser-known but increasingly important factor is the significant rise in customer acquisition costs across the insurance industry.

Over the past several years, insurers, brokerage firms, and comparison platforms have invested heavily in digital marketing channels to reach consumers online.

This competition is particularly intense on search engines such as Google, where insurance-related keywords rank among the most expensive advertising categories in Canada.

While higher marketing expenses alone do not explain premium increases, they represent an additional cost pressure across the insurance ecosystem. Like any other operating expense, these investments must be absorbed by companies seeking to maintain growth in an increasingly competitive marketplace.

Premium Increases Are Slowing in Auto Insurance

One of the most interesting findings from the Applied report is the slowdown in premium growth in Quebec.

Throughout 2025, auto insurance premium increases frequently exceeded 10% and even reached 16.4% during the third quarter of 2025. By the first quarter of 2026, the increase had fallen back to 4.0%.

This does not mean premiums are decreasing. Rather, it means that the pace of premium growth is slowing.

For Quebec consumers, this is an encouraging sign after several years of significant insurance rate increases.

Home Insurance Remains Under Pressure

A similar trend can be observed in the home insurance market.

After recording increases above 10% on several occasions throughout 2025, premium growth slowed to 4.0% during the first quarter of 2026.

Although the rate of increase has moderated, insurers continue to face rising costs related to natural disasters, building materials, and residential repairs. As a result, Quebec homeowners should still expect insurance premiums to continue rising, albeit at a more moderate pace than in recent years.

Could Insurance Premiums Continue to Increase in 2026?

All signs suggest that insurance premiums will likely continue to rise over the coming quarters.

Even though the pace of increases appears to be slowing, several structural pressures remain in place:

- Persistent inflation;

- High vehicle repair costs;

- Rising construction and building material costs;

- An increasing number of climate-related events;

- Vehicle theft;

- Growing customer acquisition costs.

For these reasons, a return to the premium levels seen before the pandemic appears unlikely in the near future.

How to Reduce Your Insurance Costs in 2026

While consumers cannot control overall market conditions, there are several strategies that can help reduce insurance costs.

- Compare quotes at every renewal: Price differences between insurers can amount to hundreds of dollars per year. Your first step when receiving your renewal should be to compare insurance quotes through ClicAssure to see whether a better rate is available.

- Bundle your policies: Combining your auto and home insurance with the same insurer often qualifies you for additional discounts.

- Review your coverage: Some coverages may no longer reflect your current needs. By using ClicAssure's online quote forms, you can obtain updated insurance pricing based on your current situation.

- Increase your deductible: Choosing a higher deductible can reduce your annual premium. However, keep in mind that this will increase your out-of-pocket costs if you need to file a claim.

- Maintain a strong insurance profile: A clean driving record and a history with few or no claims remain among the most important factors influencing insurance premiums.

Conclusion

Auto and home insurance premiums continue to rise in Quebec in 2026, but the latest Applied Rating Index data shows that the pace of these increases is slowing compared to 2025.

With annual increases of 4.0% for both auto insurance and home insurance, Quebec remains one of the least affected provinces in Canada. Nevertheless, inflation, repair costs, climate-related losses, vehicle theft, and increased competition within the insurance industry continue to contribute to higher premiums.

In this environment, consumers have every reason to compare their insurance options regularly through ClicAssure to ensure they are receiving the right coverage at the best possible price.